After years of preparation, Ireland’s new Auto-Enrolment Pension Scheme, also known as My Future Fund, will officially launch on the 1st of January in 2026.

The scheme represents a major shift in how Irish workers save for retirement. For the first time, eligible employees who are not currently paying into a pension will be automatically enrolled into a new retirement savings plan. Both the Government and the employers will contribute alongside employees, thus aiding Irish workers in their retirement planning.

Who Will Be Enrolled?

You will be automatically enrolled if you:

If you previously had a pension but are no longer contributing — and you meet the above criteria —you will also be automatically enrolled.

Those under 23 or over 60, or earning below €20,000, can choose to opt in voluntarily if they are not already part of a pension scheme.

Employees who are already contributing to a workplace pension will not be enrolled in My Future Fund.

If you are subject to PRSI Class S or M, you will not be enrolled in the new scheme.

If You Already Have a Pension

If you are already paying into a workplace pension plan, you will not be enrolled in the new scheme.

Revenue will determine whether you are a member of a pension scheme based on the November 2025 payroll submissions by the employer.

Whether the new scheme or your existing pension is better for you depends on your individual situation, income, and contribution levels. It is worth reviewing all options with a financial advisor.

Did we need an Auto-Enrolment Scheme?

With fewer than half of private sector workers currently contributing to a pension, Ireland’s private pension coverage remains among the lowest in the EU. The Automatic Enrolment Retirement Savings Systems Act 2024 was introduced to address this gap by making retirement saving the default option rather than a voluntary choice.

My Future Fund will operate on a co-contribution model, where employees, employers, and the State all pay into the employee’s pension pot.

What Happens If You Change Jobs?

The scheme follows a “pot-follows-the-member” principle i.e. if you change jobs, your pension savings move with you, so you don’t need to join a new plan. The National Automatic Enrolment Retirement Savings Authority (NAERSA) will handle the transfer automatically, ensuring seamless continuity.

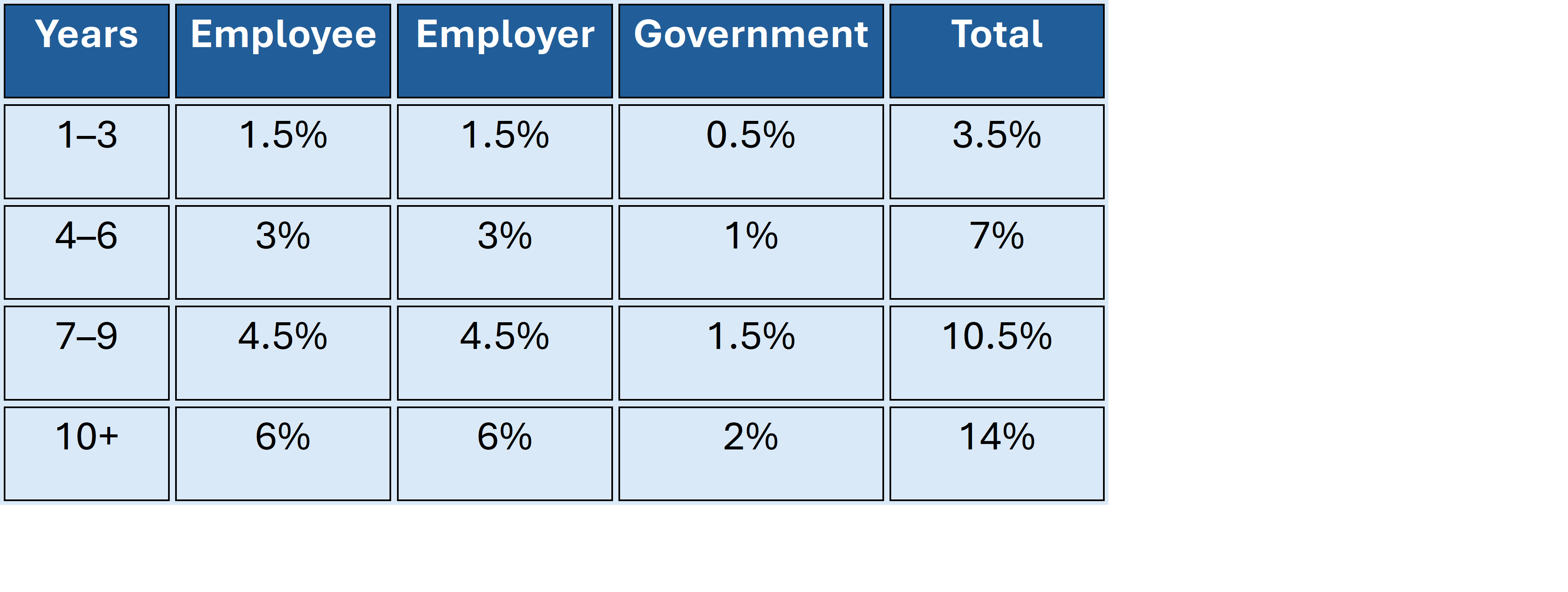

Contributions and How They Work

All three parties -employee, employer, and the State - will contribute to the pension fund. Contributions will be phased over ten years to allow for a smooth transition.

For example, for every €3 that an employee contributes, their employer will contribute €3, and the Government will add an extra €1, giving a total of €7 saved for every €3 from the employee.

Both employer and Government contributions are capped at a salary of €80,000. Employees can still contribute on earnings above that level, but employer and State top-ups will not apply beyond the cap.

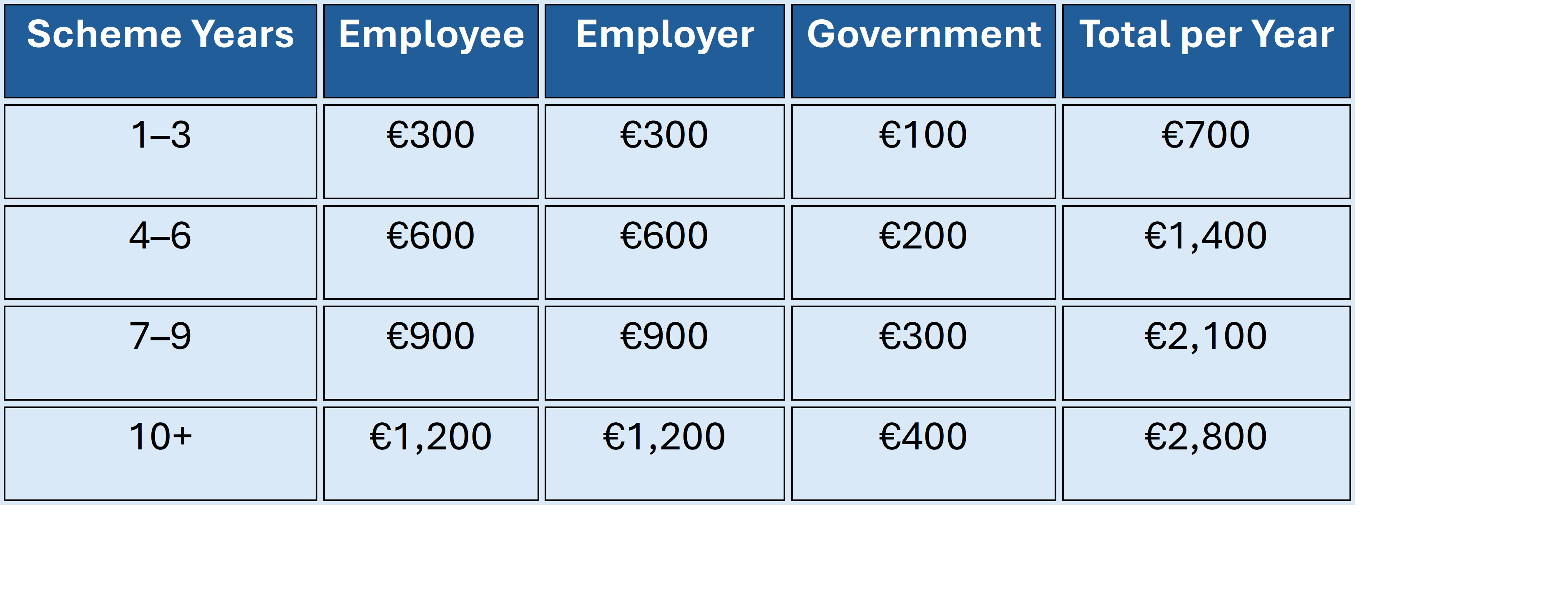

For example, an employee earning €20,000 will save as follows:

Opting Out and Suspending Contributions

Employees must remain enrolled for at least six months before they can opt out.

If you suspend or optout, you will be automatically re-enrolled after two years, provided you still meet the eligibility criteria.

Employer Obligations

Participation is mandatory for employers who have eligible employees. Employers must:

If an employer fails to meet their obligations, such as not making contributions, they may face fines, repayment requirements (with interest), and possible prosecution.

Oversight and Administration

The scheme will be administered by the newly established National Automatic Enrolment Retirement Savings Authority (NAERSA), which manages enrolments, contributions, and transfers.

The Pensions Authority will supervise NAERSA and ensure compliance, governance, and protection of member benefits.

Next Steps for Employers

With the 1 January2026 rollout date approaching, employers should begin preparations now:

✅ Identify eligible employees and assess costs

✅ Engage with payroll and HR software providers

✅ Update employment contracts and policies

✅ Communicate with staff about the scheme and its benefits

✅ Ensure budgets reflect increasing contribution rates

✅ Register as an employer on the My Future Fund website during December 2025

How PKF Brenson Lawlor Can Help

At PKF Brenson Lawlor, our tax, payroll, and business advisory teams are helping businesses prepare for the upcoming Auto-Enrolment Pension Scheme. Please get in touch.